Notes of Bute Energy and subsidiaries accounts 31/03/25 and 02/06/25 restructuring

The notes below are based on the best interpretation of restricted information available from published accounts and Company House filings and should be viewed in that light. Errors and omissions excepted.

Accounts for Bute Energy (BE) and its subsidiaries to March 31 2025 were posted on the Companies House website at the beginning of January 2026. As historic accounts they have their limitations and this is particularly so in this case because of the radical restructuring of the group that took place subsequently on June 2nd 2025 (see below). As in the previous year the results to March 25 2025 are heavily influenced by movements in the valuation of the proposed Energy Parks and Green Gen Cymru (GGC) and the, now abandoned, call option under the fair value accounting convention. The point to note is that the valuations are not based on independent or market valuations but are simply based on discounted future cash flow projections by the directors. Given the company’s poor record on past timelines, its lack of experience and the deteriorating renewables market, these should be taken with a large pinch of salt.

Leaving valuations aside, some figures from the accounts:

Development loans outstanding to CI V Dragon Lender at March 31 2025 were £143 million carrying interest at 14%.

Losses (development costs and interest payments) taken by the Energy Parks and GGC for the year to March 31 2025 were £41 million of which £20 million related to GGC

The £60 million dividend payable to Windward Energy originally announced in 2023 but then withdrawn following the initial deferred share fiasco was “paid” in January 2025 on the second attempt (see https://www.rethink.wales/defshr)

There is no specific mention in the accounts of the £600 million investment announced with much fanfare to politicians in February 2025 (albeit see 2 below re Enterprise Loan facility).

Employees including directors: BE - 56, GGC - 19. Highest paid director £541K

Political expenditure incurred (not donations) £24K

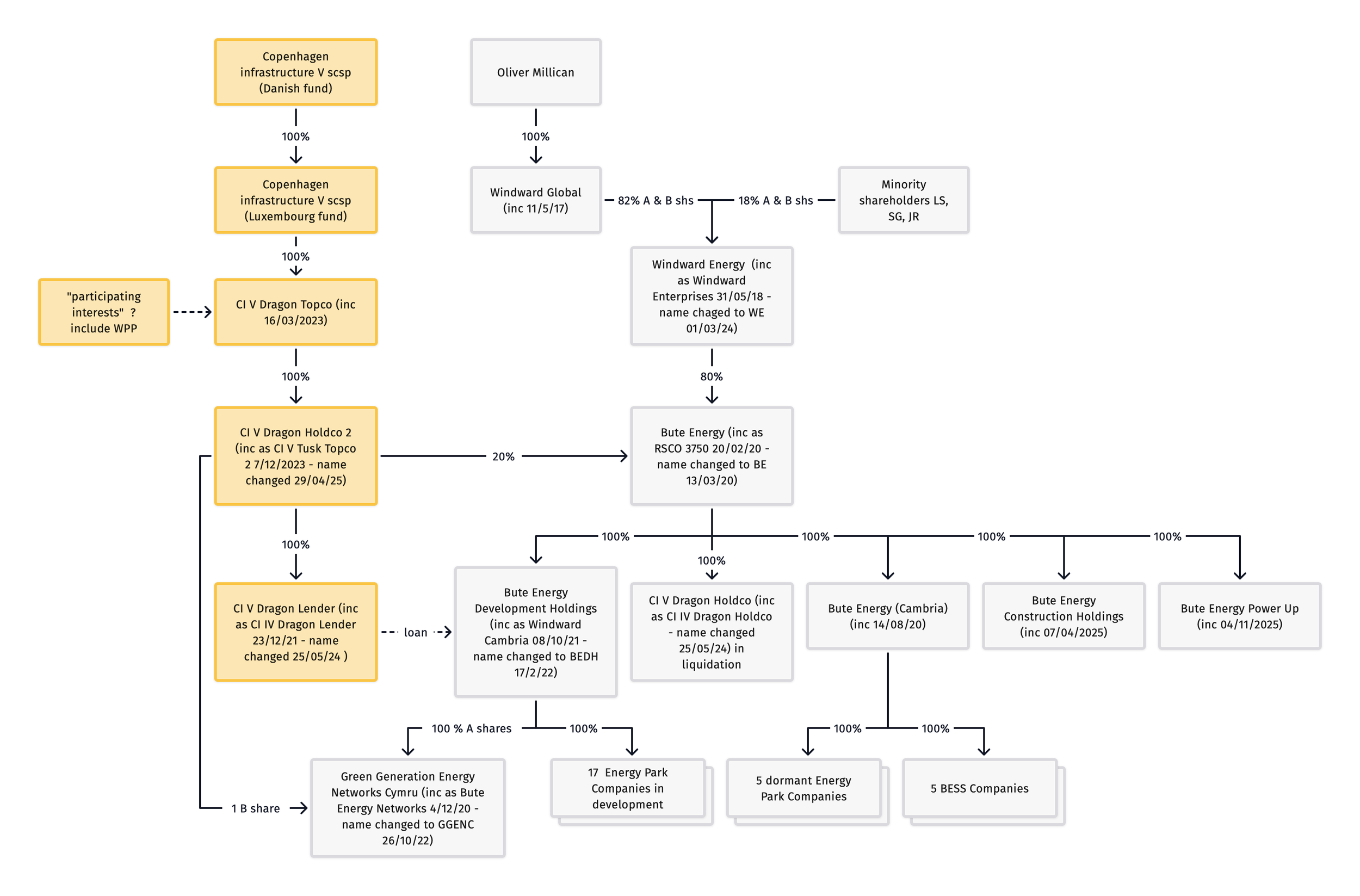

Turning to the more significant June 2nd 2025 restructuring. Although most of the changes had been picked up from Companies House postings, the post balance sheet notes in the accounts provide some additional clarity.The main changes on June 2nd 2025 were:

CI V Dragon Holdco 2 (CIDH2) acquired a 20% minority interest in BE for £40 million. On the same day BE used the proceeds plus £20 million of loan to acquire CI V Dragon Holdco (CIDH) from CIDH2. The assets of CIDH comprised the call option sold by BE to CIDH for 60 million in 2023 and the 1p B “golden” shares in the Energy Parks (not GGC). On the same day the CIP nominated directors in the Energy Park companies resigned. The effect of these transactions was to extinguish the £60 million call option and 1p B “golden” shares thus cutting any direct interest by CI V in the future acquisition or management of the Energy Parks.

An Enterprise Loan facility of £500 million with an interest rate of 12.5% replaced the existing Development Loan facility with an interest rate of 14.5%. £126 million of the Enterprise Loan facility was used to partially repay the Development loan. This was the approximate balance due to CI V Dragon Lender on 31/12/24 as per that company’s accounts. A further £68 million remained outstanding on the Development loan and it seems likely that this will also be repaid from the Enterprise Loan facility in due course. Taking these figures into account would reduce the available facility to £306 million. The Enterprise Loan is secured by registered charges against Bute Energy Developments (BED), BE and Windward Energy

6 Energy Park companies were acquired by Bute Energy Development Holdings (BED) from Bute Energy Cambria (BEC) for £17.5 million. BED also acquired £4.8 million shareholder loans from BEC. Following these transactions BEC declared a dividend of £14.1 million to BE who in turn paid a dividend of £11.4 million to Windward Energy. No accounts are yet available for Windward energy so it is not known if this was passed up to the promoters. Previous dividends paid by Windward Energy to its promoters were £14 million (y/e 31/3/23) and £58 million (y/e 31/3/24)

Note 24 in the accounts of BE refers to a partial novation of the call option “to a party that had funded the Development Loan to BED via the strategic investor”. This is possibly a reference to the “participating interests” referred to in the accounts of CI V Dragon Topco previously thought to be the Wales Pension Partnership. This is purely speculation but if it is the case it would imply that the WPP has acquired an option to buy into the Energy Parks.

A revised structure chart including the June 2nd 2025 changes above and addition of a new subsidiary “Bute Energy Power Up” in November is given below (NB this is for Bute Energy and doesn’t include companies owned by Windward Energy or higher like the hydrogen companies)

The accounts and restructuring raise the question as to what happened to the £600 million investment by CIP in Bute announced in February to much acclaim by Eluned Morgan and Ed Milliband. One suspects that the figure was always somewhat arbitrary and spun for gullible politicians (it is worth remembering that in the same announcement Stuart George claimed that 6 energy park proposals would be on the minister's desk by the end of that summer - the reality was, and remains, zero). The best guess is that the £600 million referred to the £500 million Enterprise Loan facility and “significant” minority equity investment that were part of the June restructuring. As noted above neither of these figures were as straightforward as they seem insofar as the Enterprise Loan facility was partially used to repay the existing Development loan and the £40 million investment (plus £20 million loan) appears to be a swap for buying back the call option and B shares.

The other question raised is what does the restructuring say about the relationship between CIP and Bute and the future of the Energy Parks?